14th of June 2018Every day, the mobile money industry processes over $1 billion and generates direct revenues exceeding $2.4 billion yearly, according to GSMA’s 2017 State of the Industry report. In fact, mobile money transactions in Kenya have now exceeded the country’s gross domestic product according to estimates by ICTworks. No small feat for a platform introduced a little over a decade ago in the African nation where today, five operators coexist.The poster child of mobile money success, Kenya demonstrates the massive scope for the platform as an enabler of economic growth. Mobile money platform like Alepo Digital Payments has enabled financial inclusion of millions of people by empowering them with digital financial services.Without taking away from its unparalleled success, it is important to note that mPESA – at the forefront of Kenya’s mobile money revolution – entered a largely unbanked market, with minimal competition, relied heavily on agents for transactions, and used first-generation, feature phones as the main conduit of transactions. Whether in the developed or developing world, few parallel examples remain. Today, operators must organically build complex and varied ecosystems to attract money into the platform and creating incentives to remain in the system.The key measure of how useful money is within a given mobile money ecosystem is the digital circulation ratio. A measure of how many times money is transacted before being cashed out.Simply put, increasing the digital circulation ratio involves increasing reasons to enter and stay in the system.

More options for the consumer

The most straightforward way of increasing the digital circulation ratio is to offer customers more ways to spend, giving them the incentive to use their mobile wallets more frequently for a variety of purposes. Traditional options like bill payments and money transfer remain significant, but there is also scope for more complex transactions. Some of these include:

- Buying insurance plans

- Mutual funds

- Government subsidy distribution

- Payments to enterprises (college fees, for instance)

- Saving money (micro savings)

- Microloans

Using a mobile money platform helps people build their credit scores, making them eligible for microloans through financial institutions. The score is calculated based on the transaction type, history, transaction value, location, services used, frequency of use, and so on.

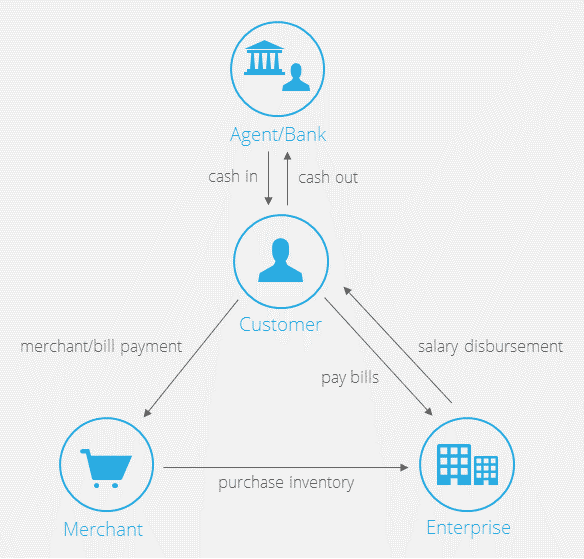

Extending services to merchants, enterprises

GSMA states that in 2017, digital circulation averaged 1.6x. However, deployments that successfully scale merchant payments have a ratio closer to 4x. Further, the most successful providers are those whose platforms offer a vast payments ecosystem; each one, on average, is integrated with seven banks, at least 90 billers and 30 organizations for bulk disbursements, and 6,500 merchants.It is business to business (B2B) and business to business to consumer (B2B2C) models that are fundamental to this success. These capabilities help expand the available vectors into the system, while providing more reasons for them to remain within. Some of these include:

- Retailer payments to suppliers: Suppliers now become part of the system by virtue of receiving payments.

- Supplier payments to enterprise: By having the option of making payments through the platform, the suppliers remain within the system instead of cashing out once they receive payments.

- Enterprises disbursing promotional cashbacks or employee salaries: Now, the enterprise has reason to continue using its money through the system.

Building such business lines requires high flexibility, not only to create different rules and policies for each business line, but also to provide business entities with internal autonomy. Flexibility provides capability, but to turn it into opportunity, the vital factor is trust. Thankfully, trust can be mediated using private blockchain.

The potential of blockchain

In creating a more diverse and complex ecosystem, it is essential to bring in major partners such as government agencies, large corporations, non-profits, and various other entities – all of which must command trust. How is trust between various entities facilitated? The answer is blockchain, where a tamper-proof ledger of all financial transactions is maintained by and shared between selected partners.At Alepo, we strongly believe that the ability to easily roll out blockchains to partners could be a game-changer. While fully decentralized blockchain-based mobile money systems have limited appeal owing to lengthy transaction times and increased costs, private blockchains can help to create highly regulated and trustworthy relationships between various major entities that participate in the ecosystem. In such an environment, the blockchain ledger is only shared with select third parties and is opaque to other participants in the system.

Diversity and innovation are the future

Mobile money systems need to create opportunities at every level and build their own ecologies, rather than relying on tapping into societal and/or economic factors. They need to have advanced partner and business channel management, flexibility in how these channels are monetized, as well as capabilities to monetize customer data itself through innovative services such as microloans. As the systems become more diverse and complex, there is a diversity in monetization methods that can be employed – analytics, advertising, revenue-share models, and more. For the success of any system, it is crucial to choose a platform that can support different business models and multilayer disbursements.

A varied ecosystem can drive up the circulation ratio